The two methods of depreciation are

-

Fixed percentage on original cost or straight line method

-

Fixed percentage on diminishing balance or written down value method

Straight Line Method

According to this method, a fixed and equal amount is charged as depreciation for every accounting period during the life time of an asset. This method is based on the assumption of equal usage of time over asset’s entire useful life. Hence, the amount of depreciation is same from period to period over the life of the asset.

Depreciation amount can be calculated by using the following formula:

-

If the asset has a residual value at the end of its useful life, the amount to be written of every year is as follows:

Depreciation = Cost of asset – Estimated net residual value / No. of years of expected life -

If the annual depreciation amount is given then we can calculate the rate of depreciation as follows:

Rate of depreciation = Annual depreciation amount / Cost of asset * 100

Advantages of Straight Line Method

-

Simple to calculate the depreciation amount

-

Assets can be depreciated up to the estimated scrap value

-

Easy to understand the amount of depreciation

-

Every year, the same amount of depreciation is debited to profit and loss account, and hence the effect on profit and loss account will remain the same.

Disadvantages of Straight Line Method

-

Interest on capital invested in assets is not provided in this method.

-

Over the years, the work efficiency of assets decreases and repair expenses increases. Therefore, there is burden on the profit and loss account.

-

Book value of the assets becomes zero but still the assets are used in the business.

Written Down Value Method

In this method depreciation is charged on the book value of the asset and the amount of depreciation reduces year after year. It implies that a fixed rate on the written down value of the asset is charged as depreciation every year over the expected useful life of the asset. The rate of depreciation is applicable to the book value but not to the cost of asset.

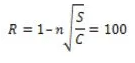

Rate of depreciation can be ascertained on the basis of cost, scrap value and useful life of the asset as follows:

Where, R is the rate of depreciation in percent, n is the useful life of the asset; S is the scrap value at the end of useful life and C is the cost of the asset.

Advantages of Written Down Value Method

-

The profit and loss account of depreciation and repair expenses has same weightage throughout the useful life of asset because depreciation decreases with an increase in repair expenses.

-

Since the benefits from asset keep on decreasing, the cost of asset is allocated rationally.

-

This method is most favorable for those assets which require increased repairs and maintenance expenses over the years.

-

This method is widely accepted under the Income Tax Act.

Disadvantages of Written Down Value Method

-

The value of assets can never be zero even though it is discarded.

-

In this method, it is difficult to calculate depreciation.

-

There is no provision of interest on capital invested in use of assets.

Difference between Straight Line and Written Down Value Method

|

Straight Line Method |

Written Down Value Method |

|

Depreciation is calculated on the original cost of fixed asset |

Depreciation is calculated on the book value (i.e. original cost less depreciation) of fixed asset |

|

Amount of depreciation remains constant for all years |

Amount of depreciation keeps on decreasing year after year |

|

At the end of the useful life of an asset, the balance in the asset account will reduce to zero |

At the end of the useful life of an asset, the balance in the asset account will not reduce to zero |

|

It is not accepted by Income Tax Law |

It is accepted by Income Tax Law |

|

It is suitable for assets which get completely depreciated on the account of expiry of its useful life |

It is suitable for assets which require more and more repairs in the later stage of its useful life |

|

Rate of depreciation is easy to calculate |

Rate of depreciation is difficult to calculate |

_20241111_110900.webp)

_20241111_111510.webp)

_20241111_111710.webp)

.webp)

_20241111_112637.webp)

_20241111_120302.webp)

_20241111_120310.webp)

_20241111_113228.webp)

_20241111_113235.webp)

_20241111_113242.webp)

_20241111_113248.webp)

_20241111_115224.webp)

_20241111_115217.webp)

_20241111_115231.webp)

_20241111_115237.webp)

_20241111_115242.webp)

_20241111_115248.webp)

_20241111_115632.webp)

_20241111_115745.webp)

_20241111_121035.webp)

_20241111_121041.webp)

_20241111_122028.webp)

_20241111_122038.webp)

_20241111_122044.webp)

_20241111_122050.webp)

_20241111_122055.webp)

_20241111_122104.webp)

_20241111_122110.webp)

_20241111_122115.webp)

_20241111_121022.webp)

_20241111_121028.webp)

_20241111_120316.webp)

_20241111_120321.webp)

_20241111_120326.webp)

_20241111_120332.webp)

_20241111_120341.webp)

_20241111_120346.webp)

_20241111_121005.webp)

_20241111_111953.webp)

_20241111_112052.webp)

_20241111_112406.webp)

.webp)

_20241111_114329.webp)

_20241111_114155.webp)

-(1).webp)

_20241111_114643.webp)

_20241111_115637.webp)

_20241111_115907.webp)

_20241111_121014.webp)

_20241111_113222.webp)

_20241111_113559.webp)